2026 Berkshire Commentary

A Year of Transition

Berkshire Hathaway’s annual meeting this past weekend reflected a company in clear transition. Newly appointed CEO Greg Abel was lighter on folksy wisdom and notably heavier on financial and operational detail. It was a different tone, but an informative one, and likely indicative of what lies ahead for shareholders.

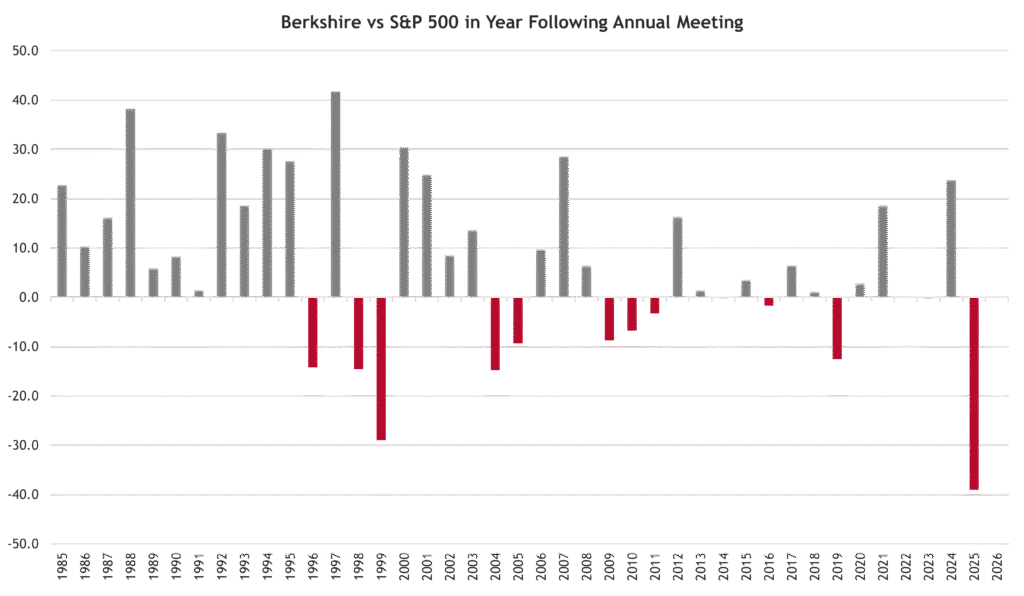

The meeting comes at a difficult moment for the stock. Since last year’s annual meeting, Berkshire has lagged the S&P 500 by nearly 40%, marking the largest relative performance gap between meetings in at least 40 years.

Source & Disclosure to Berkshire vs S&P 500

Source: FactSet. Data as of 5/4/2026. The S&P 500 Index is an unmanaged index and cannot be invested in directly. Index returns do not reflect fees or expenses. Berkshire Hathaway relative performance chart measures performance from one Berkshire Hathaway annual meeting to the next, except for the most recent period, which is shown through May 4, 2026. BRK.A was used for periods before BRK.B began trading in 1996. The spread shown represents Berkshire Hathaway performance less S&P 500 performance, with positive values reflecting Berkshire outperformance and negative values reflecting under performance. References to specific securities are for illustrative purposes only and do not constitute a recommendation. Past performance is not indicative of future results. This material is provided for informational purposes only and should not be construed as investment advice.

Limited exposure to the technology companies driving recent index gains explains part of the gap, but potential headwinds in Berkshire’s insurance operations also play a factor. Expectations for a more difficult underwriting environment in the coming years have weighed on sentiment for the broader insurance sector. Greg Abel and Ajit Jain underscored the potential headwinds, and their long-term focus on underwriting discipline.

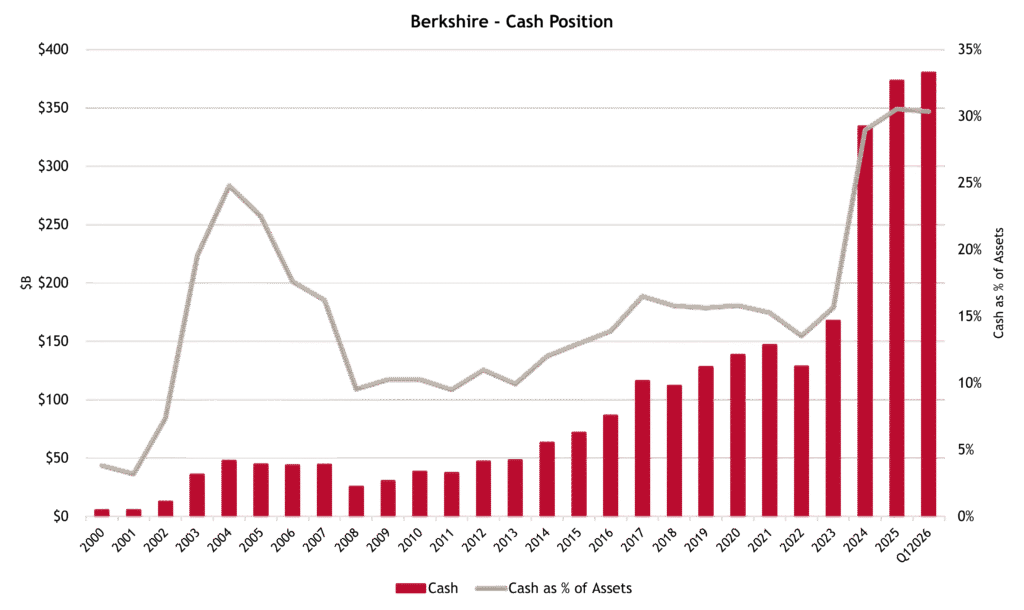

Nevertheless, Berkshire’s underlying business remains resilient, generating substantial operating cash flow across its diversified portfolio. The allocation of excess capital remains the central focus, as it has been for years, with cash and equivalents exceeding $380 billion in the first quarter. Even when adjusting for Berkshire’s size today, this represents an unusually large balance.

Source & Disclosure to Berkshire – Cash Position

Source: FactSet and Berkshire Hathaway public filings. Financial data is shown through Q1 2026; FactSet data was retrieved on 5/4/2026. Cash includes cash, cash equivalents, and short-term investments, unless otherwise noted. Cash as a percentage of assets is calculated using reported total assets. For informational purposes only; not investment advice or a recommendation to buy, sell, or hold any security. Past performance is not indicative of future results.

Cash has historically been viewed as a strategic asset for Berkshire, mitigating downside and providing upside optionality during periods of market dislocation. However, in the context of strong equity market performance, that same cash is increasingly being viewed as an opportunity cost to near-term returns, in some respects, a liability.

The current market environment is not conducive for deploying capital, with few targets that meet Berkshire’s combined requirements of scale and return. Abel reiterated Berkshire’s willingness to act decisively when the price is right, but the “strike zone” continues to narrow as the company grows larger.

We were underwhelmed by the responses regarding oversight of the public securities portfolio. The departure of Todd Combs, combined with Ted Weschler’s somewhat limited role, leaves much of the portfolio under Abel’s purview. This concentration of responsibility raises reasonable questions around bandwidth and focus, particularly given his increased involvement in operating businesses. Buffett’s public markets experience was extensive and difficult to replicate. Abel’s background is more operationally oriented, and the path forward for this portion of Berkshire’s capital is less certain for it.

With large acquisition opportunities scarce, share repurchases remain the most logical use of capital. Berkshire resumed share buybacks in the first quarter, the first such activity in nearly two years, though at a modest pace. More notably, Abel outlined a more detailed framework for assessing intrinsic value in repurchase decisions, incorporating adjusted book value, mark-to-market valuations of liquid assets, and an implied valuation of operating subsidiaries. This approach is broadly consistent with how we have historically evaluated the business.

One of the more encouraging aspects of the meeting was the expanded business update, including presentations from several operating managers that offered a rare window into the depth of Berkshire’s leadership bench. The most immediate opportunity appears to lie in improving performance at BNSF and Geico, both of which continue to trail peers on key operating metrics. Buffett’s long-standing hands-off approach to subsidiary management has been effective over time, but Abel has signaled a more engaged stance. Given the scale and complexity of Berkshire’s operations today, that shift may represent the most tangible lever for near-term value creation.

From a valuation standpoint, shares appear more reasonable today than in recent years, as evidenced by the resumption of repurchases. Still, expectations should remain grounded. Long-term performance will likely be driven by underlying business execution, with Berkshire’s size acting as a natural constraint on future growth. The more compelling case for the stock in the intermediate term lies in operational improvement and a greater willingness to hold subsidiaries to higher performance standards. Abel appears oriented in that direction.

What remains to be seen is whether the growing cash pile finds a home that justifies the wait.

Authored by: Jack Holmes, Chief Investment Officer

The views, opinions, and commentary expressed herein are for informational and educational purposes only and do not constitute investment advice or a recommendation, offer, or solicitation to buy or sell any security or investment strategy. Such views are subject to change without notice, and no representation is made as to their accuracy or completeness. Investing involves risk, including possible loss of principal. Estimates, forecasts, and forward-looking statements are not guarantees of future results.

Bridges Trust and logo reference independent services offered by Bridges Trust Company (“BTC”), Bridges Trust Company of South Dakota (“BTC-SD”) and Bridges Investment Management Inc. (“BIM”). Trust services are provided by BTC, a trust company chartered through the Nebraska Department of Banking and Finance, and BTC–SD, a trust company chartered through the South Dakota Division of Banking. BTC, BTC-SD, and certain individual clients of BIM directly utilize the investment management services provided by BIM. BIM is an investment adviser registered with the U.S. Securities Exchange Commission (“SEC”) with further information including conflicts of interest and material risks available in BIM’s ADV Brochure at www.adviserinfo.sec.gov/firm/108028 and www.bridgesinv.com. Registration with the SEC does not imply a certain level of skill or training.

Investing involves risk and the possibility of loss.

Past performance is no guarantee of future results.

CAUTIONARY STATEMENT REGARDING FORWARD-LOOKING STATEMENTS – This communication contains forward-looking statements that involve substantial risks and uncertainties. We believe it is essential to communicate our expectations to our clients. However, there may be events in the future that we’re unable to predict accurately or have no control. Actual results or other conditions may differ materially from those contemplated by any forward-looking statements, and we are not under any duty to update the forward-looking statements contained herein. Given these risks and uncertainties, readers are cautioned not to place undue reliance on such forward-looking statements.

CAUTIONARY STATEMENT REGARDING THIRD PARTY INFORMATION – This communication includes financial information, market data, statistical information, and estimates based on materials prepared by independent sources, as well as management’s own good faith estimates and analyses. We believe this third-party information to be reputable but have not independently verified it. Information based on estimates, forecasts, projections, market research, or similar methodologies or assumptions is inherently subject to uncertainties, and actual events or circumstances may differ materially from events and circumstances reflected in this information.

Additional Disclosures can be found here.